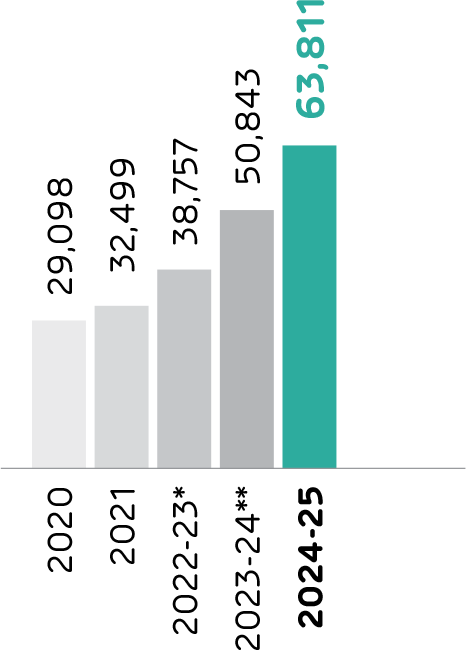

Ambuja Cements strategically harnesses its financial capital—comprising equity, debt, and diverse funding sources—to drive sustainable growth, maximise stakeholder value, and fuel expansion across various capitals. Strategic synergies and enhanced consumer engagement fuelled volume growth, increasing the net worth to an all-time high of ` 63,811 crore. The Company remains debt-free, maintaining its CRISIL AAA (stable) for its Long-Term Credit Rating and CRISIL A1+ for its short-term credit rating, a testament to its robust financial health, operational excellence and commitment to long-term value creation.

*All figures mentioned under this capital are consolidated

Focus Areas

| Growth | Margin Management and Efficiency | Financial Stability | Shareholder Returns |

|---|---|---|---|

|

Development and Key Initiatives

|

|

|

|

|

Key Performance Indicators

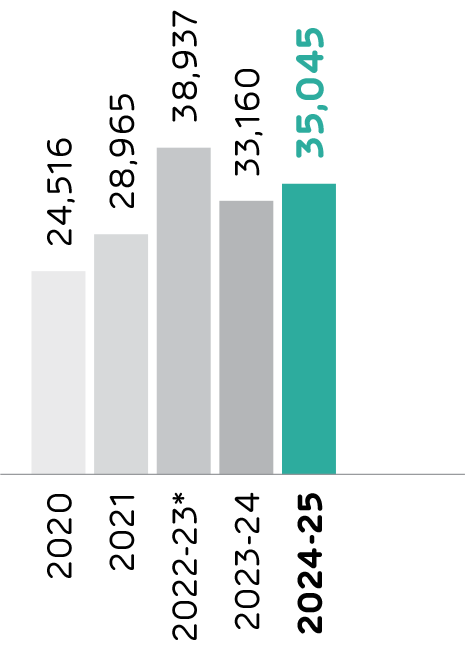

` 35,045 crore

Revenue from operations

65.2 MnT

Sales Volume |

17%

Operating EBITDA margin |

` 10,125 crore

Cash and Cash Equivalents

` 80,945 crore

Total Asset Base

` 63,811 crore

Net Worth |

` 2

Proposed Dividend Per Share in FY 2024-25

` 493 crore

Dividend Payout during the Year

13%

Dividend Payout Ratio |

Material Topics

- 1 Economic Performance

- 2 Procurement Practices

- 3 Climate and Energy

- 4 Indirect Economic Impacts

Stakeholders Impacted

-

Investors and Shareholders

Investors and Shareholders

-

Employees

Employees

-

Channel Partners

Channel Partners

-

Suppliers

Suppliers

-

Community and NGOs

Community and NGOs

SDGs Impacted

Overview

Ambuja Cements has demonstrated exceptional resilience, posting strong financial performance driven by strategic market expansion, operational efficiency, cost control, and synergies across its business. The Company’s targeted market initiatives and robust consumer engagement contributed to impressive volume growth during the year. Focused on cost optimisation, Ambuja Cements leveraged synergies within the Group to implement initiatives that reduced operating, clinker, and logistics costs, while enhancing blended cement sales, optimising energy consumption, and expanding EBITDA margins.

By optimising costs through Group synergies and business excellence initiatives, the Company’s net worth has reached an all-time high with a value of ` 63,811 crore. The Company continues to strengthen its working capital and boost treasury income to deliver positive outcomes.

Delivering Top-class Performance with Record Growth

The Technical Support team's active engagement with key influencers has strengthened the ground network, boosting trade sales volume. By providing value-added solutions beyond cement and implementing targeted branding strategies, the Company is successfully growing its share of premium products, driving higher volume growth and increased revenue.

Net Worth

(` crore)

Revenue from Operations

(` crore)

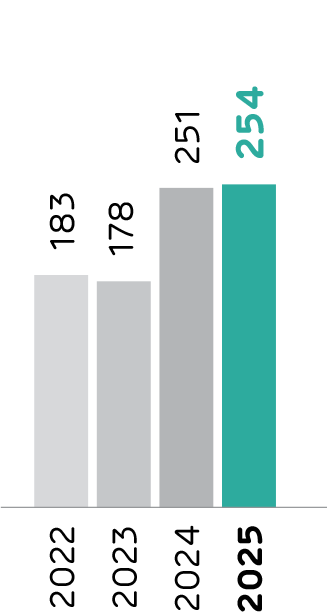

Cement Sales Volume

(MnT)

*The Company had changed its financial year ending from December 31 to March 31. FY 2022-23 was for 15 months (January 01, 2022 - March 31, 2023). Therefore, the data for FY 2023-24 and FY 2024-25 is not comparable with the figures for the 15 months year ended March 31, 2023.

**Restated, refer Note 67(g) of Consolidated Financial Statement

Delivering Results Consistently

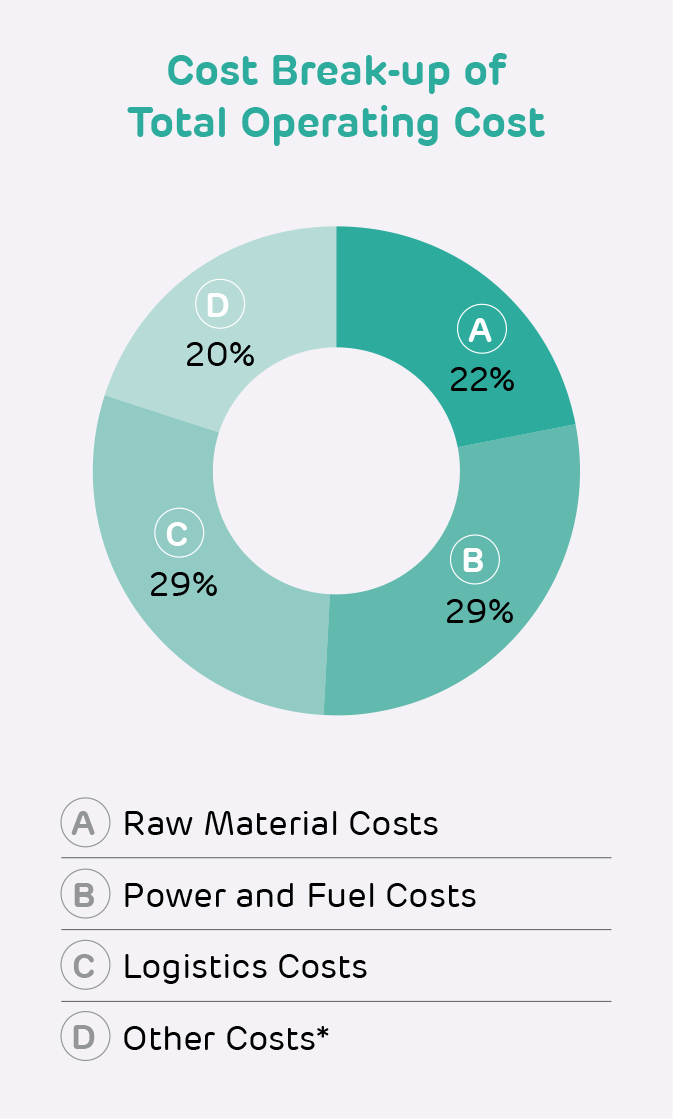

Ambuja cements is continually optimising its efficiency with the goal of significantly reducing costs to ` 3,650 (PMT) by FY 2027-28. Approximately 65% of total costs are supported by synergies with Group Companies in sectors where Adani is a market leader, reinforcing the cost-reduction strategy. The Adani Group's established presence in power, coal access, and port infrastructure provides significant advantages. These synergies facilitate the achievement of economies of scale, improved logistics efficiency, and a steady supply of raw materials. An accelerated Capex programme, funded through internal accruals, is in place, with Group synergies acting as a key enabler of growth. Higher trade sales, premium product volumes, and value-added solutions, combined with cost reductions and improved efficiencies, have enhanced margins and driven strong volume growth at a premium price.

Ambuja Cements is leveraging digitalisation, automation, AI, sustainability and lead distance reduction to drive logistics cost efficiencies. With an expanding presence along India’s coastline, the Company operates 17 sea-based terminals and Grinding Units, including 11 strategically located Bulk Cement Terminals (BCTs). Specialised BCFC rakes and EV trucks enhance volume handling and reduce supply chain emissions while further lowering costs. Additionally, with 40% of its Fly-Ash requirements secured through long-term agreements, Ambuja Cements ensures robust material security to support its cost leadership strategy.

*Other Costs include: Other expenses; Employee benefits expenses; Changes in inventories of finished goods, work-inprogress, and stock-in-trade.

Earnings

The Company reported an operating EBITDA of ` 5,971 crore, resulting from a reduction in several expenses such as power, fuel and freight, amongst others. The net profit for the year stood at ` 5,158 crore, with a net profit margin of 15%.

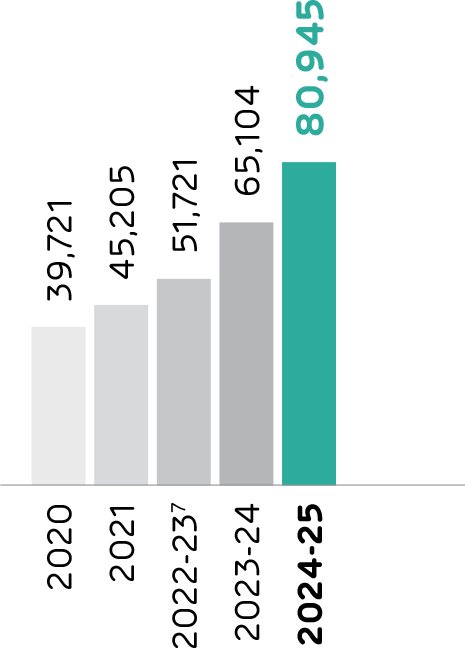

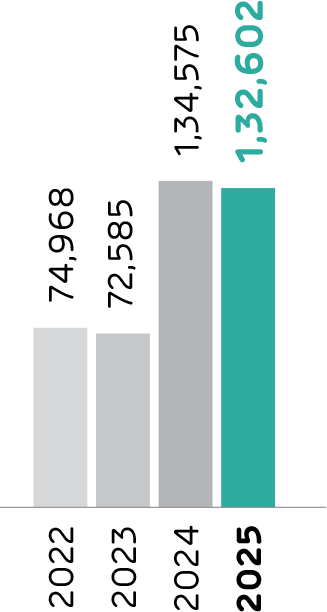

Assets

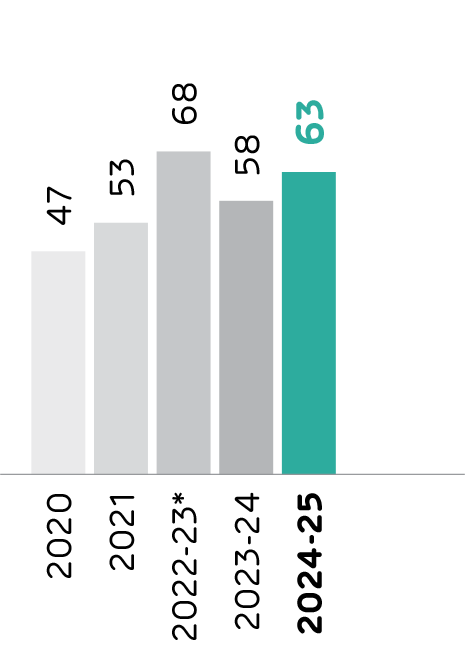

As of FY 2024-25, Ambuja Cements reported a total asset base of ` 80,945 crore, reflecting a steady increase from the previous year. Current assets constituted approximately 24% of the total, providing the Company with robust liquidity for ongoing operations and expansion plans.

The asset growth was primarily driven by strategic investments in its manufacturing capacities, sustainability initiatives and infrastructure development. The Company continues to benefit from strong synergies with the Adani Group, particularly in power, coal access, and logistics, which have further enhanced its asset utilisation. With a debt-free status and a focus on efficient capital allocation, Ambuja Cements is well-positioned to maintain its growth trajectory and financial stability moving forward.

Growing Asset Base

(` in crore)

7 Note: The Company had changed its financial year ending from December 31 to March 31. FY 2022-23 was for 15 months (January 01, 2022 - March 31, 2023). Therefore, the data for FY 2023-24 and FY 2024-25 is not comparable with the figures for the 15 months year ended March 31, 2023.

Robust Capital Management Program ensures Growth with Credit Discipline

CRISIL Ratings has reaffirmed the Company’s Long-Term Credit Rating at the highest level of AAA/Stable and its Short-Term Credit Rating at A1+ for bank loan facilities. These ratings reflect the Company's strong financial stability, its capacity to meet financial obligations, and a solid risk profile.

AAA(Stable)

Long-Term Credit Rating

A1+

Short-Term Credit Rating

Cement Capacity

(MTPA)

Focused Expansion

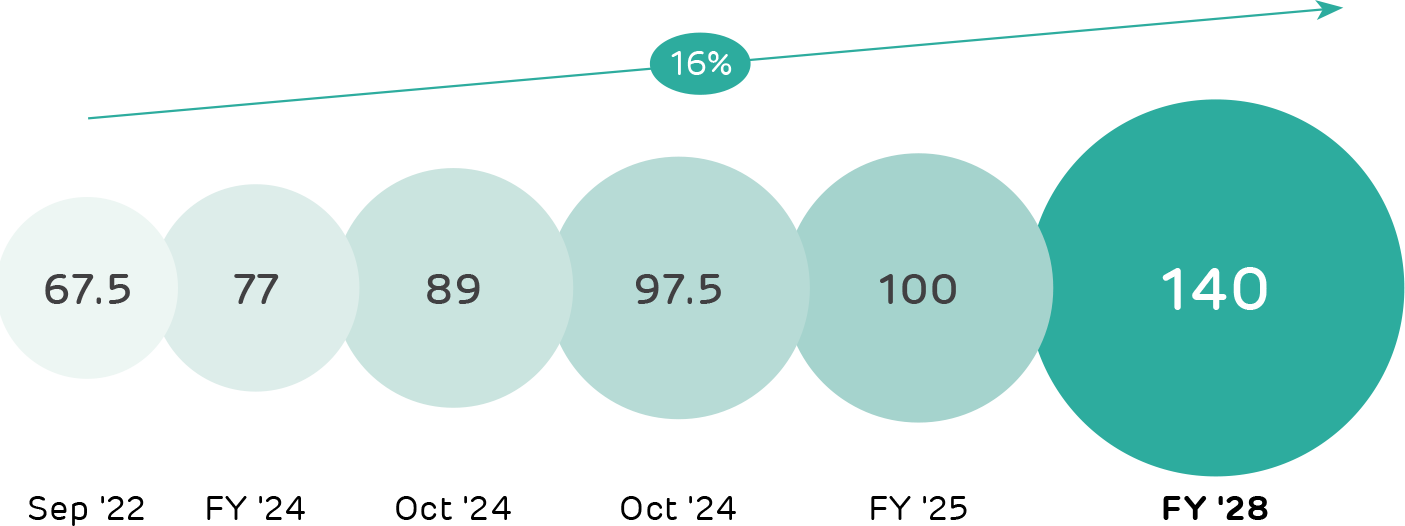

As Ambuja Cements is progressing on its journey to achieve a remarkable 140 MTPA capacity by FY 2027-28, the Company is strategically leveraging financial capital to fuel its growth ambitions. The Company is utilising operating cash inflows and internal accruals to fund its expansion projects, ensuring a strong balance sheet and prudent capital allocation.

Ambuja Cements' organic growth strategy includes a balanced mix of greenfield and brownfield projects. The Company is investing ` 1,600 crore in a 6 MTPA cement grinding unit in Bihar. Ongoing expansion projects for FY 2024-25 include 4 MTPA clinker capacity at Bhatapara, 2.4 MTPA capacity at Sankrail and 1.6 MTPA at Sindri that are in the advance stages of completion and commissioning. In all, there are 12 projects across various locations which will add 11 MTPA clinker capacity and 19 MTPA cement capacity by end of FY 2025-26. The Board has also approved additional cement grinding units at various locations, which will add an additional 21 MTPA cement and 16 MTPA clinker capacity. The overall capacity went over 100 MTPA in FY 2024-25, 118 MTPA by FY 2025-26 and well on track to achieve targeted capacity of 140 MTPA by FY 2027-28. With further projects in advanced stages of execution, we are on the cusp of significant growth, the Company aims to increase our cement capacity to 140 MTPA by FY 2027-28.

Sustainable Investment Strategy

In the past year, the Company has strengthened its commitment to sustainability through strategic investments designed to reduce environmental impact and promote eco-conscious practices. By focusing on energy efficiency and increasing the use of renewable energy, the Company is positioning itself for lower power costs in the future, aligning with its goal to enhance green energy usage across all operations.

Additionally, Ambuja Cements has stepped up its waste management efforts, embracing circular economy principles to decrease reliance on virgin materials and reduce waste. This not only minimises environmental impact but also enhances margins. These efforts are integral to the Company’s overarching strategy to achieve Net Zero emissions by 2050. Notably, Ambuja Cements is one of two Indian cement companies along with its subsidiary ACC to have undergone Net Zero target validation through the Science Based Targets initiative (SBTi), further solidifying their leadership in sustainable practices. The validation for ACC has been completed.

Investor Relations

Ambuja Cements is dedicated to building stakeholder confidence by continuously enhancing transparency in shareholder communication and providing consistent business updates on recent developments to all its stakeholders. At the Company, investor relations (IR) is a strategic management function that effectively conveys the equity story and investment proposition to institutional investors and shareholders. Ambuja Cements is placed in the 'Good' category by Institutional Investor Advisory Services (IIAS) in the Indian Corporate Governance Scorecard (2024).

To maintain a strong relationship with investors, the Company engages with them through a variety of platforms. These include Annual General Meetings (AGM), quarterly and annual results presentations, and meetings with Chief Investment Officers (CIOs) and High Net-Worth Individuals (HNIs).

Furthermore, the Company participates in investor conferences both domestic and overseas, organises investor roadshows, events, plant visits and presents detailed investor reports. Throughout the year, important business updates are proactively communicated to a wide network of opinion-makers through various channels, including emails, social media platforms like WhatsApp and LinkedIn, one-on-one calls and stock exchange disclosures. The Company has also raised disclosure standards with initiatives such as the Tax Transparency and Sustainability Report, BRSR, high-quality investor presentations, strategic rationale decks for key acquisitions, and acquisition-focused conference calls. These various modes of interaction are conducted quarterly, annually, or as required, ensuring that stakeholders are kept informed of the Company's progress and future outlook.

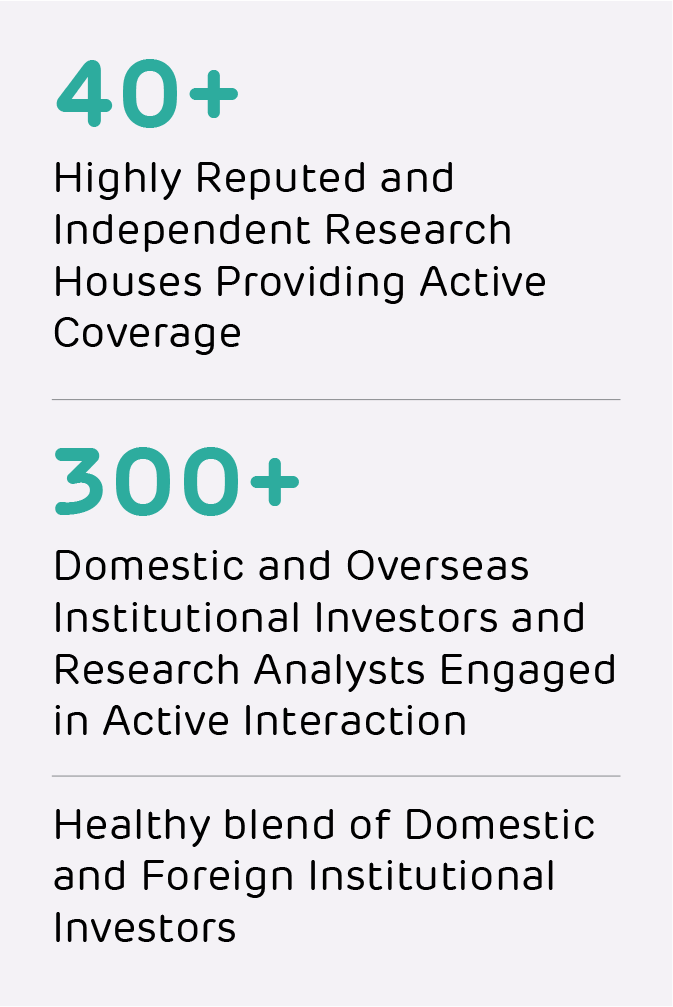

The Company engaged with over 300 investors and research professionals across different geographies through investor conferences, one-on-one meetings and non-deal roadshows.

Investors have key expectations regarding the Company's performance, including sustainable growth, attractive returns and profitability. Additionally, they emphasise the importance of risk management, corporate governance and clear policies. Investors also seek better disclosures, transparency and credibility in the Company's financial reporting.

In response, the Company is committed to providing regular financial disclosures and governance updates. The Company also prioritises effective risk management, maintains an open line of communication through its Investor Relations function, and ensures timely and transparent communications with all stakeholders to address their expectations and foster long-term trust. The continuous efforts of the Investor Relations team are helping the Company to enhance their capital market visibility, build stakeholder confidence and significantly reduce response times to stakeholder queries.

Leveraging Group Synergy

Ambuja Cements leverages the synergies of the Adani Group by aligning its strategic initiatives with the Group’s broader capabilities. By tapping into shared resources, advanced technologies, and robust financial strength, Ambuja Cements enhances operational efficiency and drives sustainable growth. The collaboration facilitates cost optimisation, streamlined supply chain and logistics, and access to innovative digital solutions, ultimately strengthening the Company's market position.

Merger and Acquisitions (M&A) and Integration

Ambuja Cements Limited is committed to becoming the lowest-cost cement producer while maintaining superior quality. Strategic acquisitions have played a pivotal role in expanding the Company's capacity and bolstering its competitive advantage. By integrating these assets, Ambuja Cements has optimised its supply chain, reduced operational costs, and strengthened its market position. Since the integration of Ambuja Cements into the Adani Portfolio, a total of 32.9 MTPA (including Orient's under-construction projects) capacity has been added through strategic acquisitions. These acquisitions, valued at a cumulative `24,896 crore, include Orient Cement Limited, Penna Cement Industries Limited (PCIL), Sanghi Industries, Asian Fine Cements, Asian Concretes & Cements, and a grinding unit in Tuticorin. These assets have been efficiently integrated with Ambuja Cements Limited.

The acquisition of Orient Cement Limited (OCL) has taken Ambuja Cements' cement capacity to 100+ MTPA, reducing overall lead distances and logistics costs for the cement business and improving market share in their core markets. Ambuja Cements' strategic acquisitions have bolstered its capacity and market presence, providing a competitive advantage while optimising the supply chain, reducing costs, and enhancing its footprint. With a range of CAPEX and OPEX initiatives in place, the Company is accelerating its journey towards cost leadership, further solidifying its position as an industry leader.

Enterprise Value of M&A

Acquisition of Penna Cement Industries Limited

The acquisition of Penna Cement Industries Ltd. marks a key milestone in the Company’s growth journey, further reinforcing its leadership across India and enhancing its presence in South India. This strategic move opens up new avenues for synergies, innovation, and value creation, setting the stage for continued success.

With Penna Cement now integrated into the Adani portfolio, the Company’s manufacturing capacity has been significantly expanded, adding four integrated plants, two grinding units, and five bulk cement terminals (BCTs) and an under-construction integrated unit at Marwar. This expansion boosts its footprint across eight states, with a particular strengthening of its position in the Eastern and Southern regions. The BCTs offer a competitive advantage by improving access to maritime routes, opening up new markets like Sri Lanka. This acquisition has also propelled the Company’s Southern market share from 7% to 15%, advancing its ambitious targets of reaching 118 MTPA by FY 2025-26 and 140 MTPA by FY 2027-28.

Acquisition of Orient Cement Limited

Ambuja Cements has announced the acquisition of Orient Cement Ltd (OCL) for an equity value of ` 8,100 crore, a strategic step aimed at surpassing 100 MTPA in operational capacity. This acquisition includes a 46.6% stake in OCL, acquired from its current promoters and certain public shareholders, all funded through internal accruals. The deal adds 8.5 MTPA to the Company's cement capacity, with a further 8.1 MTPA ready to be executed. Additionally, it unlocks 6 MTPA of potential clinker capacity in North India, leveraging OCL’s limestone reserves in Rajasthan.

OCL brings highly efficient assets, including railway sidings, captive power plants, renewable energy facilities, waste heat recovery systems (WHRS), and alternative fuels and raw materials (AFR) capabilities, which will bolster Ambuja’s footprint in strategic markets. This acquisition is expected to increase the Company’s pan-India market share by 2%.

Hedging

To manage financial risks stemming from market volatility, Ambuja Cements implements comprehensive hedging strategies. These strategies effectively mitigate exposure to fluctuations in commodity prices, exchange rates, and interest rates, ensuring financial stability and protecting overall performance.

Financial Engineering

Through innovative financial strategies, Ambuja Cements optimises its capital structure, maximises shareholder value, and mitigates financial risks. By effectively utilising financial instruments, capital markets, and structured transactions, the Company navigates complex financial landscapes, driving sustainable growth and strengthening resilience in the face of market uncertainties.

Tax Transparency

Ambuja Cements has implemented a dedicated tax governance framework to manage its tax affairs with integrity and responsibility. This framework ensures timely compliance with tax obligations, building stakeholder trust and protecting the Company’s reputation. A specialised team, guided by subject matter experts, follows international best practices and standard operating procedures to maintain consistency and transparency across all operations.

The Legal, Regulatory, and Tax Committee at the Board level oversees the effectiveness of the tax compliance programme, while the Board of Directors serves as the final authority on tax matters, underscoring the Company’s commitment to ethical, compliant, and professional tax practices.

Enterprise Value Creation

The Company has transitioned from a traditional finance approach to a more strategic business finance model that focuses on long-term value creation and true business partnership. Committed to delivering superior stakeholder value, the Company efficiently manages its financial capital. Through a unique and disciplined approach to financial management, optimal use of resources, and the adoption of innovative practices, the Company has achieved faster project completions and made thoughtful capital allocations, all contributing to sustained value creation for stakeholders.

Enterprise Value Framework

- Growth-oriented

- Gatekeeper for Compliance

- Broader Approach covering ESG

- Multi-stakeholder Engagement

- Focus beyond Cash Flow and Liquidity Management

Economic Value Created

(` in crore)

| FY 2024-25 | FY 2023-24 | |

|---|---|---|

| Direct Economic Value Generated | 37,699 | 34,326 |

| Revenue from Operations | 35,045 | 33,160 |

| Other Income | 2,654 | 1,166 |

| Economic Value Distributed | 35,129 | 32,415 |

| Cost of goods sold8 | 16,483 | 15,195 |

| Employee Wages and Benefits | 1,403 | 1,353 |

| Payments to Providers of Capital | 493 | 496 |

| Payments to Government | 16,648 | 15,284 |

| Community Investments | 102 | 87 |

| Economic Value Retained | 2,570 | 1,911 |

8 Cost of Goods sold includes: - (i) Cost of material consumed, (ii) Purchase of stock-in-trade, (iii) Changes in inventories of finished goods, work-inprogress and stock-in-trade, (iv) Power and fuel, (v) Consumption of stores and spares, and (vi) Consumption of packing material.

Market Capitalisation

Ambuja (standalone)

BSE 100 Ranking Company